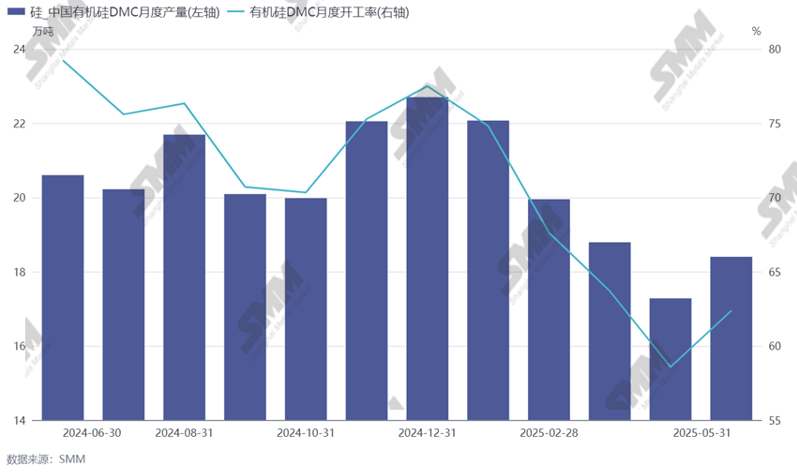

SMM News on June 6: According to SMM statistics, domestic silicone production in May increased by 6.48% MoM from April, with the operating rate rising to 62.37%. During the month, leading enterprises conducted large-scale maintenance, but the load of some other enterprises' facilities slightly increased. As a result, the operating capacity decreased, while the actual production increased. Although some facilities will still be under maintenance in June, it is expected that the production schedule will continue to rise due to the impact of increased load.

Figure: Trend of Silicone DMC Production

Review of the market in May: During the month, leading enterprises in north-west China conducted large-scale shutdowns for maintenance, causing a significant decline in the industry's operating rate. However, due to the subsequent cancellation of some tariffs in the trade war, the downstream high-temperature adhesive market improved, leading to an increase in DMC order intake compared to the previous period and a decrease in DMC inventory levels. Coupled with the gradual resumption and reaching of full production of previously maintained production lines, production began to increase from mid-May, resulting in an overall increase in DMC supply in May.

Figure: Trend of Silicone Polysiloxane Inventory

Production Schedule Expectations for June: In June, the maintenance of leading enterprises is expected to end. A monomer enterprise in north China will conduct comprehensive maintenance of its facilities. The monomer operating capacity will experience both increases and decreases, but the overall load rate is expected to rise. It is optimistically expected that DMC production in June will increase to nearly 200,000 mt.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)